The elusive VC edge

“What’s your edge?” No question has been asked by VC (Venture Capital) managers as often as this. And with good reason. Just as any business, if you want to attain market dominance, having a clearly defined edge that aligns with every action and feature of your business is essential.

But in venture, the question often prompts answers that point in thousands of directions. Managers may point to their value-add, their track record, their unique thesis, or something else. From speaking to more than 350 VCs on the EUVC podcast, investing in a few of them, and collaborating with Floww, we’ve come to believe that the best answer encompasses all of these elements and more.

The answer to “what’s your edge” can take anything from 5 minutes to 60 minutes – or rather, 60 days of deep due diligence. Because this is exactly what any LP (Limited Partner) is looking for to define, test and underwrite. So, in the LP meeting, the art lies in knowing how deep to go, where to focus (which can vary greatly depending on the LP) and knowing how to effectively articulate your narrative. For this whitepaper, we’ve partnered with our good friends at Floww and Foundamental to draw a roadmap to defining and testing your edge.

For this whitepaper, we’ve partnered with our good friends at Floww and Foundamental to draw a roadmap to defining and testing your edge. We cover:

1 — The roadmap to defining and testing your edge

2 — The meta discussion of the roadmap

3 — The application of the roadmap in two podcast episodes with two European VCs – one newly minted manager, the other a well-established rising star and exit of the year winner in 2024 at the European VC Awards

Before diving in, let us caveat. Many LPs have been taught to ask this question, but few know exactly what answer they’re looking for. When fundraising, you’re often the most prepared person in the room – at least when it comes to venture capital. So don’t go all meta and describe this framework in a fundraising call, rather, use this to inform how you build your narrative.

1 — The roadmap to defining and testing your edge

Before diving into the full whitepaper, start with our cheat sheet for a quick overview of the key points. Then, explore the following pages for a deeper dive into each topic.

For a more interactive experience, go to section 2 and check out our podcast episode where the authors—Patric from Foundamental and Andreas from EUVC—discuss the framework and its practical applications in detail.

1.1 Unique empathy for an underserved market

Knowing your market in depth is more than just a nice-to-have; it unlocks unique insights that inform every action in your firm. Whether it’s a framework like Mike Maples Jr.’s at Floodgate, centred on inflection points & insights, or the philosophy of our co-authors at Foundamental around project-based industries such as construction, the key is having enough knowledge to cultivate a unique perspective that founders value—so much so that they choose you.

And this is only the beginning. A clearly defined, intimately understood market allows you to shape your firm in perfect sync with what that market needs. More on this in the next chapter on building the experience required to win.

Unique empathy: When I speak with new managers and LPs seeking venture allocations, I often start with a straightforward, perhaps even provocatively simple, statement: I look for managers where I can draw a direct line from their experience to running a VC firm with their specific thesis and strategy. VC is tough; the numbers speak for themselves. Most managers don’t generate returns that justify the risk. To outperform, a manager must bring unique capabilities; if they’re not top-notch in this regard, the fund is likely a trivial pursuit for both manager and allocator.

For professional LPs, 99% of VCs are accessible. These LPs benchmark managers not against local peaks but global standards. Managers aiming to build a lasting firm should hold themselves to this level—otherwise, VC is simply a low-fee business built on empty carry dreams. In venture, hope is not a strategy.

Am I being too hard? I don’t think so. Venture has a problem: a long tail of managers who simply don’t perform. If these managers could self-identify, both LPs and VCs would benefit. How would this impact founders? Short-term, it might reduce available funding, but long-term, it could lead to a gold rush as VC—appealing even to less sophisticated LPs—would outperform and expand in reach.

What does unique empathy look like at the emerging manager stage? It’s about highly relevant operator or founder experience, a track record of on-thesis investments, a powerful and relevant network, and enough expertise to not only be contrarian but also right. Europe has several managers who exemplify this. For established funds, this alignment grows more complex, but you can see how the most successful firms evolve strategically to serve their target founders exceptionally well. Great examples include, Seedcamp’s latest publicly shared fundraising deck or our episode with Will Prendergast, founding GP of Frontline.

1.2 Building repetitions

LPs seek firms that raise from a position of strength and build towards market dominance. When you’re raising, it’s essential to do so with a foundation of experiences that have given you significant reps within your focus area. But it’s equally important to structure your firm to accelerate your expertise and installed base in the areas that matter most to your founders—and faster than your competitors.

This is where Floww’s data-driven approach comes into play. Floww provides a powerful infrastructure that allows investors to track and measure key performance indicators, automate fund administration, and gain real-time insights into portfolio health. By leveraging Floww’s platform, VCs can not only define their edge but also continuously refine and validate it against market realities.

A great example of how VCs are using Floww to enhance their operations is the Pages feature. This tool allows a VC to create a single space to share updates with their investors, build a more transparent narrative around their portfolio’s performance, and ensure they remain aligned with their key stakeholders. Additionally, built-in analytics offer VCs valuable data about investor engagement, helping them refine their approach to communication and reporting.

In the episode accompanying this White Paper, Patric from Foundamental shares how every activity they undertake is designed to build repetitions within the project-based industries.

Source: Foundamental

Ultimately, VCs who succeed in today’s landscape do so by combining deep market insight with real-time data intelligence. With Floww, investors gain the ability to benchmark, communicate their value proposition effectively to LPs, and build a truly differentiated investment strategy.

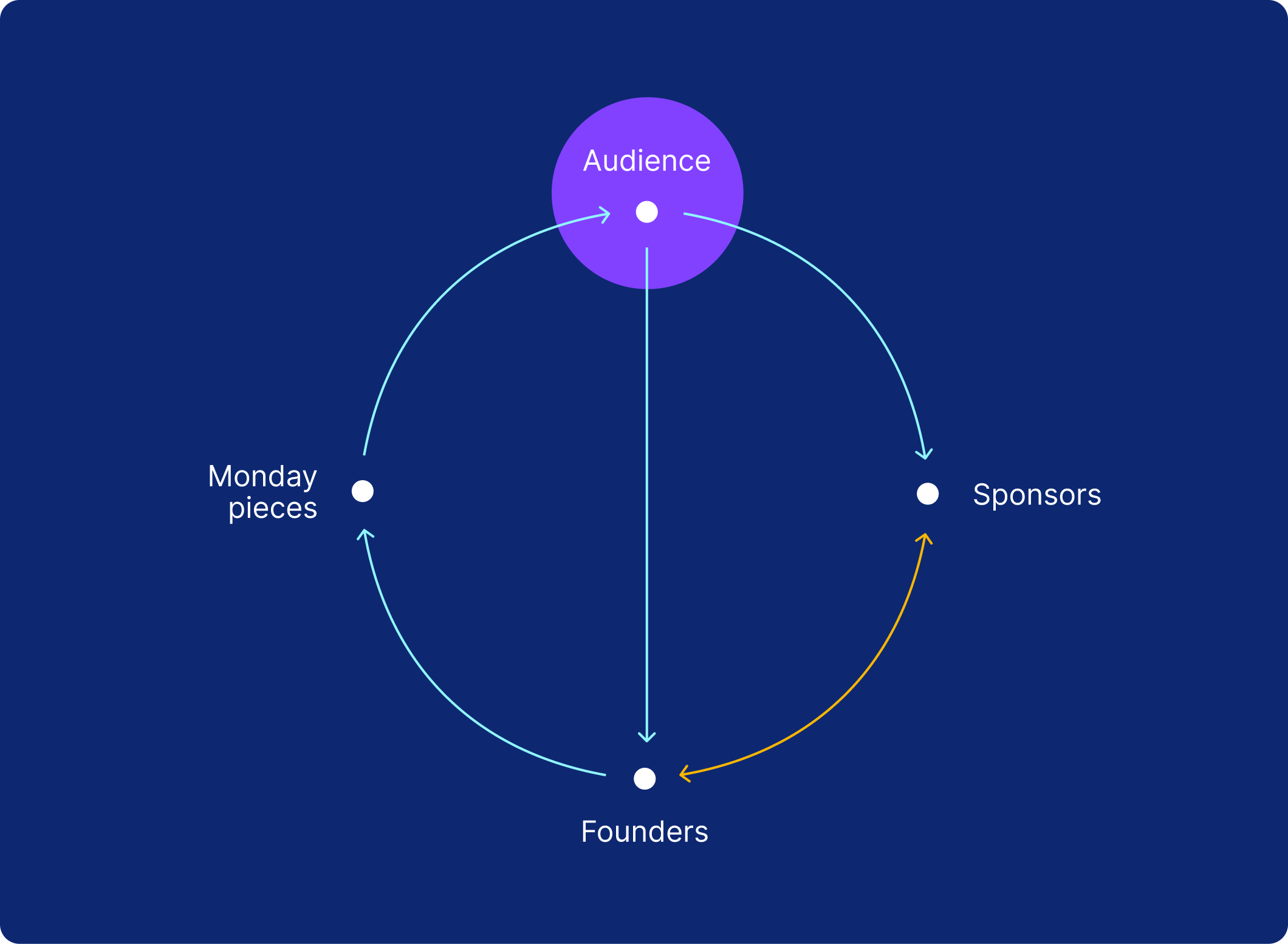

1.3 Distribution flywheel

VC is a game of reach—reaching founders, co-investors, and LPs. Yet, for most firms, resources are limited, making operational efficiency critical. That’s where creating flywheels between core activities and marketing efforts becomes essential. For a true deep dive on Flywheels in venture, a great reference piece is Jake Singer’s analysis of “Not Boring”-author and VC Packy McCormick’s flywheel

Another great example of how a distribution flywheel can be built and communicated to LPs is Seedcamp’s as they describe it in their fundraise deck for Fund IV (publicly accessible on slideshare). The section opens with a simple statement encapsulating everything:

“The more we invest, the stronger our reach.”

This message is supported by powerful visuals (see the carousel below). When assessing “reps done,” this is the kind of alignment you want to see across the firm. Every activity—whether reviewing deals, meeting founders, or closing LPs—should sharpen your edge, driving you from a position of advantage to one of market dominance.

Source: Seedcamp

Source: Seedcamp

Source: Seedcamp

Source: Seedcamp

1.4 The Arena

It’s ironic how many VCs expect founders to deliver a precise grasp of market size and timing but then turn to their own fundraise decks with a generic “we’re investing in B2B SaaS across Europe” and call it a day.

If you’re a 10x angel, decacorn founder, or an Index alum, that might slide. But for most, you’d be far better off showcasing a well-founded, contrarian view of the market backed by data and insights—something that builds real conviction that you just might be right.

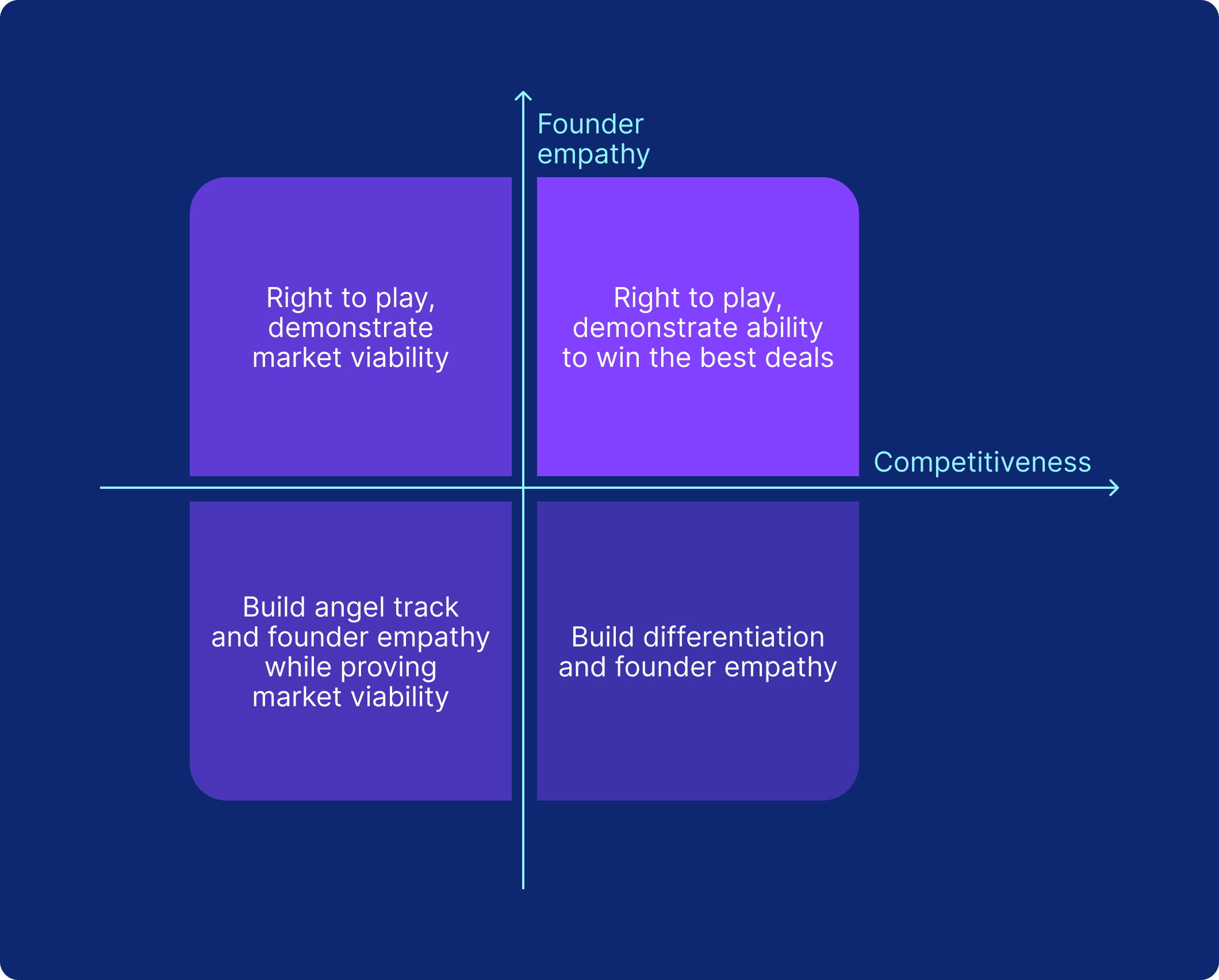

There’s no universal formula here—what makes a compelling VC thesis varies by investor. Generally, though, the sweet spot combines an external market opportunity (mixing verticals, geography, tech trends, and timing) with an internal advantage (a unique blend of empathy, expertise, and distribution).

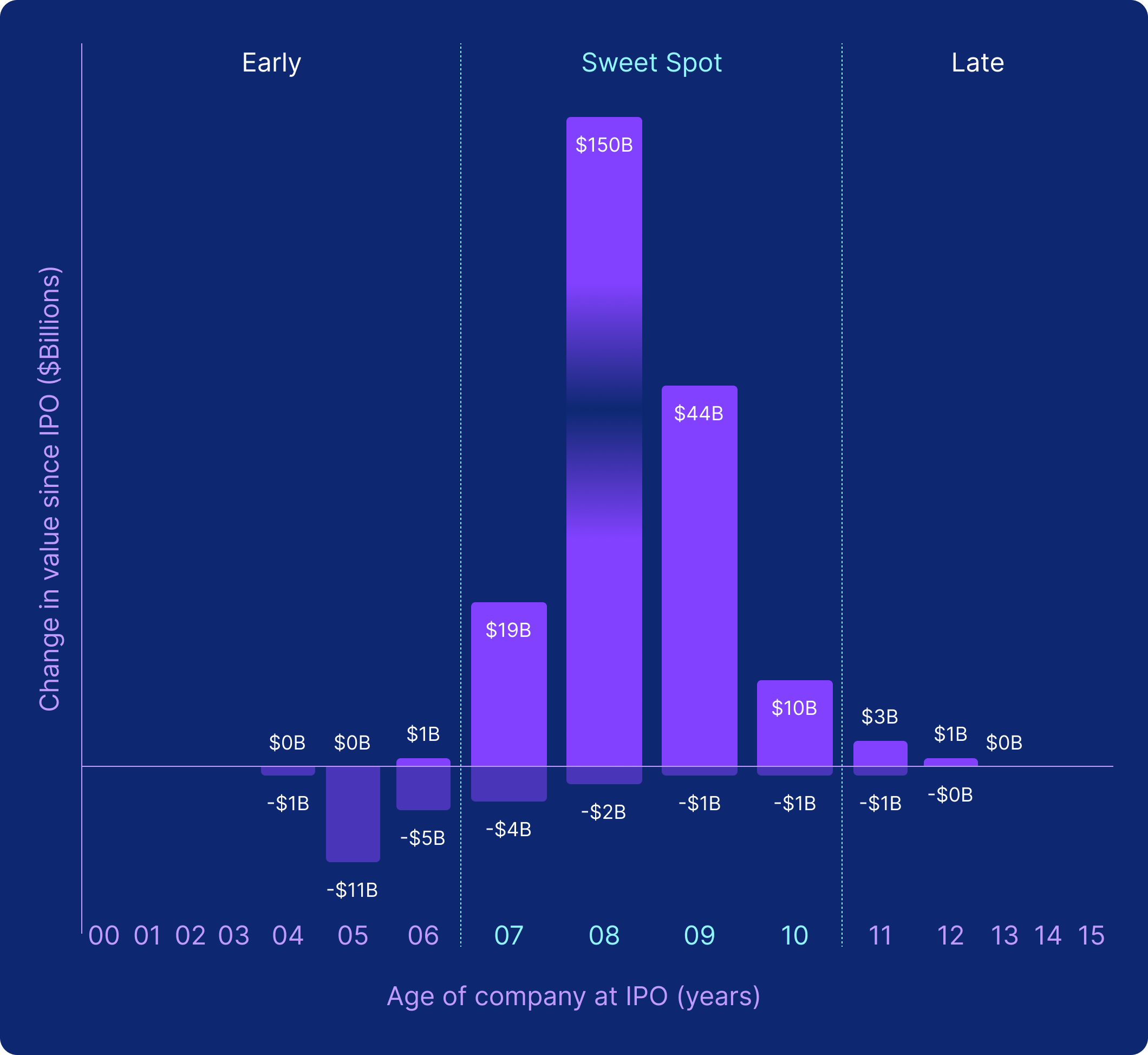

In Play Bigger (2016), Al Ramadan, Dave Peterson, and Lucas Ramadan introduced the “6-10 Law,” which outlines a common trajectory of startups moving from idea to IPO within 6 to 10 years. It’s a pattern that aligns with the venture model, almost as if validating it—though any deviation can significantly impact our industry.

Inflection Theory

Another influential VC author, Mike Maples Jr., further explores this in Pattern Breakers (2024), where he dissects how Inflection theory drives VC outcomes. In my humble opinion, one of the most important reads you as a VC can read when building your thesis. Not to apply his framework, but to inspire a similar verbalization of your own.

Inflections, along with Insights that harness them, empower startups to develop Pattern Breaking ideas that radically change how people live. Founders discover these powerful insights by Living in the Future.

Foundamental exemplifies this in the chart to the left, where they show how project-based industries, such as the construction market, are mirroring the trajectories of more established venture capital sectors—illustrating how a new wave is primed for them to ride. As an LP, seeing hundreds of VC decks all describing similar looking career trajectories, investment strategies and track records, insights like this may just be what piques my interest enough to want to know more.

1.5 The Players in the Arena

VC is a team sport. We take minority stakes, so taking a company from inception to IPO alone isn’t possible. That’s why demonstrating to LPs that you understand the players, know how to navigate the arena, and have earned respect among peers is essential. Sophisticated LPs scrutinize this closely, using it for benchmarking, references, and to identify alternative investments—your competition for their capital as they seek the top contender.

Take Isomer Capital, a leading European early-stage Fund of Funds, as an example of diligent “arena” assessment before (re-)committing to a fund as described in a past episode we did with them.

For them, it’s not just about past performance—it’s about dissecting the conditions that created those returns and assessing whether they still hold. They dig into questions like: Have market dynamics shifted? What’s changed in the early-stage pricing environment or in the strength of founder networks? Is the original team still in place? For Isomer, these aren’t just routine questions but essential in ensuring they’re investing in a team that still has what it takes to perform.

Moreover, Isomer believes that private markets require an exhaustive, forward-looking approach. They meet and speak with as many market participants as possible, recognizing that backward-looking data can only serve as a guide, not a guarantee. Their diligence goes deep, balancing every promising new team they meet against rigorous standards to ensure it’s not just a good fit personally but genuinely strategic for their portfolio. They ask themselves, Is this fund truly unique in the context of our current exposures, or is it redundant given our geographic or sectoral coverage?

Isomer’s approach also involves a retrospective lens, analyzing gaps in their portfolio. They reflect on what they might have missed in certain regions or sectors over the past 5-10 years and evaluate who could cover those areas now. For Isomer, understanding the competitive landscape, potential new players, and previously overlooked areas is key to refining their strategy and ensuring they’re partnering with the best possible funds.

Why blue ocean strategies are tough in venture: VC thrives in sectors that are not only growing but also have competition. In a slow-growing market, opportunities are scarce. In a fast-growing yet under-competitive space, LPs lack benchmarks and worry about the financing risk of your vertical. This dynamic is a big reason we see such persistent herd behavior in the industry.

1.6 The Path to Returns

This isn’t the place for an in-depth dive into investment strategy, portfolio modeling, or track record—entire books cover these topics, and, of course, there’s an excellent series of masterclasses by your EUVC friends 💖. However, it’s worth mentioning that the ultimate measure of your edge and approach is your ability to maximize the probability and minimize the time to high DPI. And demonstrating as part of your fundraising materials that you master this.

As Fred Destin put it in a past EUVC episode:

“Just be a student of venture and portfolio construction and know what a Montecarlo simulation is or whatever method you want to use to talk about portfolio diversification. But you have to be a student of that stuff because if you don’t demonstrate to LPs that you’re a good money manager they won’t give you money.”

Even with all the characteristics discussed earlier, lacking a solid understanding of this aspect makes you a risky bet for any LP.

So, what’s the “right” strategy? There’s no universal answer. Concentrated portfolios work; broad portfolios work. Zero follow-on strategies work; 70% reserve allocations work. The key is knowing what aligns with your target opportunities, investment approach, and firm goals. It’s about making thoughtful, consistent decisions with the capital entrusted to you by LPs.

To attract LPs, prove through your track record, strategy, and edge why you’ll secure exposure to alpha.

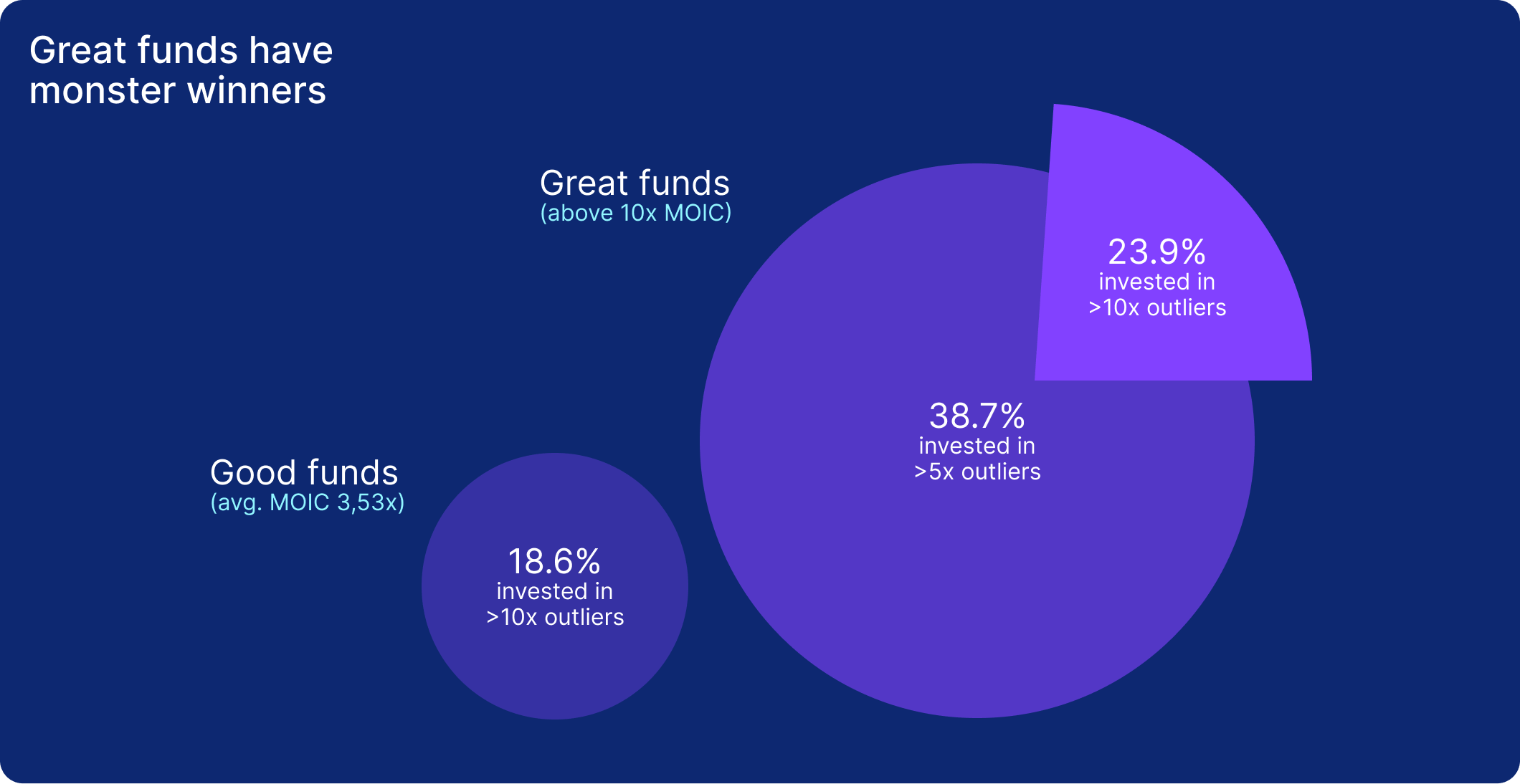

A critical aspect of this is ensuring thoughtful exposure to your outliers. In a 2024 study, Primary analyzed Stepstone’s data, finding that “Great Funds” (10x+ returns) allocated 38.7% of capital to 23.1% of investments that delivered 5x+ and 23.9% to those yielding 10x+. By contrast, “Good Funds” (3.53x average) only allocated 18.6% of capital to 14.4% of their 5x+ investments. The takeaway? A primary driver of great funds’ returns was their concentrated capital in winners. If the “Good Funds” had similarly allocated, they’d have achieved a >8x MOIC.

In the end, you need to demonstrate a thoughtfully designed investment strategy aligned with a track record of investments and exits aligned with it.

1.7 Investment Discipline

A well-known business proverb says strategy is less about what you do and more about what you don’t do. In venture, this means staying in your lane—doing deals that leverage your edge, build your reps and flywheel, and fulfill the strategy LPs backed you to execute.

That said, venture is deeply FOMO-driven. Logo hunting is tempting, can grow AUM, and places you among the top names. But what does a small check in a massive round at the edge of your thesis really deliver for LPs? Often, not much.

Then again, even the smallest stake in the next Facebook could be transformative, and many top investors champion being price-disciplined but also knowing when to break that rule.

The takeaway? It’s complicated. That’s why you need clear principles and parameters for handling edge cases and big opportunities. Many LPs want insight into the thinking, processes, and actions you’ll take when those pivotal moments arise.

In parallel, managing LP relationships and keeping your investors updated on your journey is more important than ever. This is where Floww comes in, allowing you to seamlessly share content, updates, and even manage investor reporting—all in one place. With built-in analytics, you can track engagement and see the real-time impact of everything you share with your network. Keeping investors informed and staying connected is paramount, using effective tools helps to build trust and demonstrate transparency.

2 — Hear from the Authors: Patric and Andreas Dive Deep into the Whitepaper’s Framework

Watch Andreas Munk Holm from EUVC and Patric Hellerman from Foundamental delve into the Edge framework—pay close attention, as while we co-developed this framework, we each have our own perspectives on its finer points, just as any LP you meet will. In VC, there’s no single truth. So watch, reflect, and come to your own conclusions.

3 — The application of the roadmap in two podcast episodes with European VCs

3.1 Jörg Binnenbrücker on EUVC: Applying the Edge Framework to Capnamic Ventures

In this episode of EUVC, we welcome Jörg Binnenbrücker, Founding and Managing Partner of Capnamic Ventures. With a €190 million Fund III and a core focus on seed and Series A investments, Capnamic is a leading player in digital tech across Europe with a particular emphasis on the DACH region (Germany, Austria, Switzerland). Known for backing high-growth startups like LeanIX, Staffbase, Adjust, Getsafe, dexory, Accure, and Marktpilot, Capnamic has become a trusted partner for founders and LPs alike.

We’re excited to dive into how Capnamic embodies the Edge framework, which combines a deep understanding of their market, strategic portfolio construction, and disciplined investment practices. Listen in as Jörg shares his insights on building a high-performing VC firm that delivers real value to founders, co-investors, and LPs alike.

The Future of Venture Capital Capnamic’s structured approach highlights a crucial trend in modern venture capital: the fusion of market-specific expertise with disciplined investment practices. As the ecosystem evolves, Floww is playing an increasingly important role in bridging the gap between founders and investors. Floww’s data-driven infrastructure complements Capnamic’s methodical investment strategy by providing deeper insights, streamlining due diligence, and facilitating transparent investor-founder relationships.

In an increasingly data-centric investment landscape, firms that combine structured discipline with digital enablement will be best positioned to drive superior returns and build resilient portfolios. The future of venture capital is not just about capital deployment—it’s about harnessing the right insights to make smarter, more strategic decisions.

3.2 Lorenzo Franzi on EUVC: Applying the Edge Framework to Italian Founders Fund

In this episode of EUVC, we welcome Lorenzo Franzi, a founding partner of Italian Founders Fund. Focused on building up Italy’s tech ecosystem, Italian Founders Fund combines regional specialization with a dynamic support network, positioning itself as a transformative player for Italy and the Italian diaspora. With six investments so far, Italian Founders Fund targets early-stage founders, leveraging an extensive network of Italian entrepreneurs and industry professionals to drive meaningful growth.

We’re excited to explore how Italian Founders Fund applies the Edge framework, bringing empathy for Italy’s unique market, rigorous execution, and a focus on long-term impact in venture. Lorenzo dives into his experiences and shares how Italian Founders Fund is set up to support a new generation of Italian tech founders.

Italian Founders Fund’s application of the Edge framework showcases a methodical, high-impact strategy for building Italy’s tech ecosystem. With a clear focus on Italian founders, disciplined execution, and a hands-on LP network, the fund is positioned to generate strong returns while fostering Italy’s venture ecosystem.

Leveraging tech like Floww’s, these firms can deepen their strategic capabilities, providing VCs and LPs alike with the tools to collaborate more efficiently, track portfolio performance in real-time, and align better with their long-term goals. This approach ensures that the Edge framework remains as relevant as ever in the current venture landscape, enhanced by the digital tools that define the future of venture capital.